A few months ago, BofA’s Michael Hartnett coyly suggested that AI is a “baby bubble” just waiting, like HR Giger’s alien, for its moment to spawn into fully-grown form (with several million human shorts as hosts). Today, the coyness is gone, and in his latest Flow Show note titled aptly enough “A short history of bubbles”, Hartnett – perhaps after observing the recent move in names like ARM and SMCI – is no longer shy about calling the parabolic spade a spade and details not only a “short history of bubbles” but where the Magnificent 7 fits in.

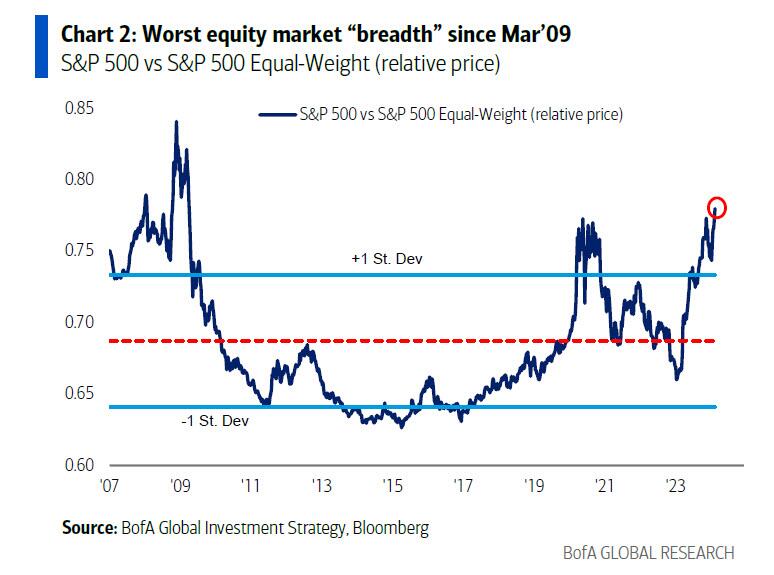

But before digging in, Hartnett starts off by highlighting the indispensable “glue” of any bull market, and hence bubble, namely credit… and sure enough there is plenty of glue right now with Investment Grade spreads “tight-as-a-drum”, and close to post-Covid lows of 86bps (despite a record $310BN in YTD issuance). Yet if credit is rock solid (and after 2020 when the Fed ended up buying IG ETFs making it clear the Fed would never allow credit to lock up again, why not?) the same can not be said for equities, where the bull market is so narrow: just the top 5 stocks account for 75% of all S&P YTD gains, and just the top 3 tech stocks account for 90% of tech sector YTD gains. Indeed, as shown in the next charts, US equity breadth is now the worst since March 2009, when the S&P troughed its post-Lehman crash around 666.

In this light, it is hardly surprising that corporate bonds and tech stocks are the consensus “all-weather” assets which go up no matter whether the news is good or bad. Indeed, inflows to both are on course for blowout years: YTD annualized $0.5 trillion to IG bonds, and $85 billion to tech sector funds).

So speaking of bubbles, there is plenty of material to work with: a pure reflection of human nature… and greed… bubbles have a long, illustrious history: from the South Sea, to the Mississippi monopolies of 1710s, the Dow in the Roaring 1920s, gold in the inflationary ‘70s, Japan in the ‘80s, internet in the ‘90s, China in the 2000s, the Great Bond Bubble 2014-20, crypto, FAANG, tech disruptor derivatives; and so on…

… one thing is certain: no two bubbles alike (as Hartnett suggests “try blowing a couple yourself“) but similarities to gauge the Magnificent 7 today are catalyst, price, valuation & “price of money.”

So without further ado, here is Hartnett’s “Short History of Bubbles”, a quick and dirty comps vs today’s Magnificent 7:

- Catalyst: bubbles driven by technological innovation, new geographical sources of growth, and very crucially central bank easing; AI bubble was kick-started by Fed response to SVB and ChatGPT…just as Plaza Accord kick-started Japan, LTCM the internet, 9/11 the housing bubble of 2000s, COVID ($30tn of policy stimulus) crypto and so on; even Mississippi and South Sea Company bubbles caused by amendment to English usury laws in 1714 which forbade lending rates over 5% as UK & France needed to borrow to finance ceaseless war…no different today;

- Price: bubbles (obvs) mean huge trough-to-peak asset gains; 140% gain in Magnificent 7 past 12 months closing in on 180% rise in Dow Jones in 1920s & 150% for both Nifty 50 in ‘70s & Japan stocks in ‘80s, but not quite 190% gain of internet bubble (everyone’s fave comparison) nor 230% surge in FAANG stocks from COVID lows; note exponential price gains (“velocity” or big deviation from moving averages) another classic bubble symbol…Magnificent 7 currently 20% above 200dma vs the 30% “oversold” metric of 9 equity manias covered in Table 2;

- Valuation: trailing PE for Magnificent 7 currently 45x…it ain’t cheap but true that bubble highs have seen dafter valuations… 54x for Nifty Fifty, 67x for peak Nikkei in ’89, 65x for Nasdaq Composite in 2000 (and staggering 205x for Nasdaq 100), 60x in 2021 for peak FAANG;

- Bonds: direction of bond yields key bubble metric as “abnormality” of bubble infects other assets & economy; in 12 of 14 observed bubbles, bond yields rising as bubble peaks/pops; tightening financial conditions via policy or rising real rates (if central banks have no backbone) the constant catalyst for the “pop“…4% real rates popped internet bubble, 2% popped Chinese stock bubble, 3% popped subprime, surge in real rates from -100bps to +150bps in ’21/’22 popped bitcoin, FAANG, ARKK; given significantly higher levels global debt today versus history 10-year real rates, currently 2%, likely need to rise to 2.5-3% to end AI, Magnificent 7 mania.